Your grandparents always seemed to have money when it mattered. No apps. No spreadsheets. No financial advisors. Turns out their "old-fashioned" habits weren't outdated at all — neuroscience and behavioral economics are now proving these methods work better than most modern tools. Here's what they knew that Wall Street charges you to learn.

Grandma Never Needed a Budget App

You remember the person. Maybe it was your grandmother, maybe an uncle or your mom. They never checked an app or watched a finance YouTube channel. Yet somehow, when the car broke down or school supplies were due, the money was there. No panic, no credit card scramble — just a calm walk to a drawer, an envelope, or a jar on the counter. It looked effortless, almost magical.

Here's the thing: it wasn't magic, and it definitely wasn't primitive. Behavioral scientists and financial researchers are now confirming what these quiet money managers knew all along — their habits were neurologically and psychologically brilliant. One of the simplest? Labeled envelopes full of cash.

The Envelope System Still Works

You've probably seen those envelopes — maybe in a kitchen drawer, maybe in a purse with the flap worn soft from handling. Groceries. Gas. Rent. Fun money. Each one labeled in pen or marker, each holding exactly what could be spent that month. When the grocery envelope was empty, you stopped buying groceries until next month. No overdraft, no guilt, no math. Just a physical boundary you could feel between your fingers.

That feeling part matters more than anyone realized back then. There's something about physically touching and releasing money that changes how your brain processes a purchase — and researchers have measured exactly how much.

Why Cash Registers Hit Different

Here's where it gets wild. Researchers at MIT and Carnegie Mellon put people into brain scanners and watched what happened when they paid for things. Paying with physical cash literally activated the brain's pain centers — the same regions that fire when you stub your toe. Cards and apps? Barely a flicker. That neurological "ouch" made cash users spend 12-18% less on identical purchases, not through willpower but through biology.

Your parents weren't being old-fashioned with those envelopes. They were using a neurologically superior spending system without knowing the science behind it. But the brain tricks don't stop at the register — there's another old-school habit that hijacks impulse buying before it even starts.

The "Sleep on It" Spending Rule

Here's a rule you can start using right now: if it costs more than $50 and you don't absolutely need it today, sleep on it. That's it. Wait 24 hours before buying. Your grandparents did this instinctively — they'd say "let me think about it" and walk away. Turns out, research shows that roughly 70% of impulse purchases lose their appeal after just one night. That desire you felt in the store? It was mostly adrenaline, not actual need.

Now here's why this matters even more today: companies have spent billions engineering one-click buying specifically to eliminate your cooling-off period. Every "Buy Now" button is designed to prevent you from sleeping on it. Try the $50 rule this week and watch how many purchases simply evaporate overnight. Speaking of things quietly draining your money while you're not paying attention — when was the last time you actually read a bill?

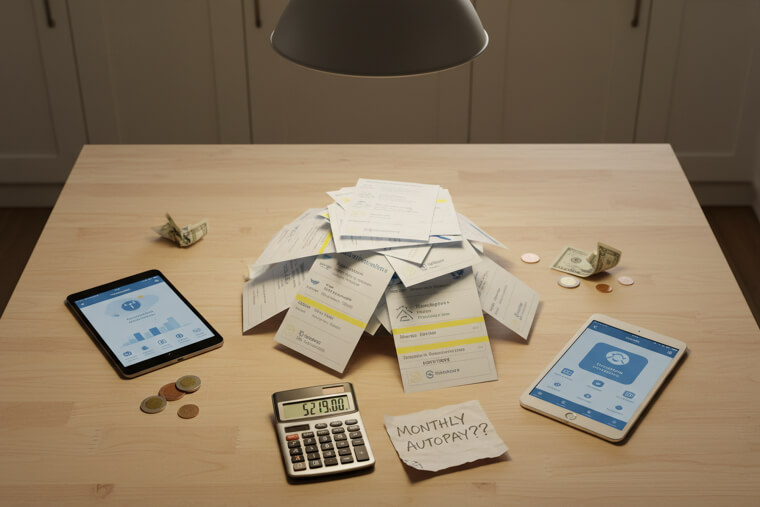

Paying Bills the Day They Arrive

Here's something nobody talks about: your grandparents didn't pay bills immediately because they were disciplined. They did it because leaving an unopened bill on the counter felt like leaving the stove on. Open it, write the check, done — mental clutter gone. But that habit had a hidden superpower. Every single bill got read. Every line item got scanned. Every price increase got noticed. Now think about your autopay setup. When was the last time you actually looked at your electric bill or streaming charges?

Studies show people on autopay are significantly less likely to notice when companies quietly raise prices — and most do, regularly. That "convenience" could be costing you hundreds annually without a single notification. And the real number? It's worse than you think.

How Autopay Quietly Drains You

Here's the number that should make you uncomfortable: the average American spends $219 every month on subscriptions they've forgotten about or barely use. That's not a typo. Streaming services, fitness apps, cloud storage upgrades, meal kits you tried once — they're all quietly billing you while you scroll past the notifications. That adds up to over $2,600 a year. Enough for a family vacation. Enough to fully fund an emergency savings account. Gone, because nobody's opening the envelope anymore.

When your parents manually reviewed every bill each month, they created a natural audit cycle that caught exactly this kind of silent drain. No app reminded them — the habit itself was the reminder. So what did the most financially sharp people use instead of apps to track their daily spending? A tool that costs about two dollars.

One Notebook Exposed Every Leak

Here's your challenge: grab a small pocket notebook — the kind that fits in your back pocket — and for one week, write down every single purchase. Coffee, parking meter, vending machine, everything. Don't use your phone. Actually write it by hand. Neuroscience explains why this works: the physical act of writing engages your brain's encoding process far more deeply than reading a screen notification. You don't just see the number — you feel it. Your hand remembers what your eyes forget.

Most people who try this discover at least $200 in spending they had zero awareness of. Not big purchases — tiny ones that slipped past every app and alert. That daily iced coffee. Those "small" Amazon orders. The notebook doesn't judge. It just shows you the truth. And once you see those leaks, you'll understand why the humble coin jar might be the most underrated savings tool ever invented.

The Coin Jar Was Stealth Savings

Here's something behavioral economists are just now catching up to: that dusty coin jar on your grandmother's kitchen counter was a sophisticated savings device. They call it "micro-saving" now, and apps like Acorns charge monthly fees to do digitally what that jar did for free — collect spare change automatically. The psychology is identical. Small amounts removed from circulation, barely missed, quietly compounding. But here's the number that surprises everyone: families who kept a coin jar consistently accumulated $300 to $800 every single year without ever feeling like they were saving.

No account minimums. No subscription fees. No app permissions. Just gravity and glass. The secret wasn't the coins themselves — it was that the saving was painless, invisible, almost accidental. That concept of effortless saving will come back later in a big way. But first, there's another old-school cash trick that silently stopped people from overspending — and psychologists now have a name for it.

Why They Carried Small Bills Only

Financial insiders know a trick your grandparents practiced without ever reading a study. Before shopping, they'd break large bills into smaller ones at the bank. Seemed like a quirky preference — but behavioral economists have a name for it: the denomination effect. Research shows people are dramatically more reluctant to break a large bill than to spend the same amount in smaller ones. A $100 bill feels like a possession. Five $20s feel like spending money. Same value, completely different psychological weight.

Next time you hit an ATM, try requesting small bills instead of large ones. You've just installed a free spending brake that no app can replicate. Speaking of shopping, there's another old-school rule that saved families far more than just time.

Grocery Lists Saved More Than Time

Your grandparents had an ironclad rule: never walk into a grocery store without a handwritten list. And never, ever grab something that wasn't on it. Research backs them up — unplanned grocery trips cost 40 to 60 percent more than planned ones. Modern delivery apps make it even worse, suggesting add-ons and "frequently bought together" items designed to inflate your cart.

Here's your two-step action. First, check your pantry before writing the list — you'll skip things you already have. Second, leave your phone in the car when you shop. No app upsells, no digital distractions, just you and the list. What you won't buy might surprise you. And that savings mindset extends well beyond the kitchen — especially when something breaks.

They Fixed Things Instead of Replacing

Here's a number that should stop you mid-scroll: the average American household spends over $1,500 every year replacing items that could be repaired for a fraction of the cost. A cracked phone screen, a wobbly chair, a dryer that stopped heating — previous generations didn't even consider throwing these away. They resoled shoes, patched jeans, rewired lamps. Repair was the default, not the exception. Somewhere along the way, we decided fixing things was harder than buying new ones.

The irony? It's actually easier now than it was for your grandparents. YouTube has free repair tutorials for virtually everything — from washing machines to winter coats. The skills aren't lost, just forgotten. And that repair-first mindset didn't stop at the workbench. Inside the kitchen, an even simpler habit was quietly saving families thousands.

The "Use It Up" Kitchen Rule

Think about what you threw away this week. Stale bread that could've become breadcrumbs or French toast. Chicken bones perfect for homemade broth. Vegetable scraps that simmer into rich soup stock. Your grandparents looked at "leftovers" and saw ingredients. We look at them and see trash. The cost of that shift? American families waste roughly $1,800 in food every single year. Let that land for a moment — that's a monthly car payment vanishing into your garbage can, twelve times a year.

The old kitchen rule was brutally simple: use what you have before you buy anything new. No meal-planning app required, just eyes and intention. That wasted $1,800 stings — but wait until you hear what store credit cards are quietly costing the people who fall for that "save 15% today" pitch.

Why They Hated Store Credit Cards

Here's what financial advisors will tell you off the record: store credit cards are the single worst deal in retail. Your grandparents didn't need that insider knowledge — they felt it instinctively and said no every time. Here's why they were right. Store cards carry average APRs between 28 and 30 percent, among the highest in all of consumer lending. That cheerful "save 15% today" pitch at the register is banking on one thing — that you'll carry a balance. And most people do.

When that happens, one month of interest erases an entire year's worth of those so-called discounts. The math is brutal and non-negotiable. So next time a cashier offers you that deal, picture your grandmother shaking her head. She knew. Now you know the exact numbers behind her instinct. Speaking of cash and spending — what happens when you pay for dinner with paper bills instead of plastic might genuinely surprise you.

Paying With Cash Changes the Meal

Here's the counterintuitive twist nobody expects: spending less at restaurants actually makes people enjoy their meals more. A study on dining habits found that customers who paid cash ordered fewer appetizers, skipped dessert more often, and spent 25% less per meal than card-payers. But they didn't feel deprived — they reported equal or higher satisfaction. Why? Handing over physical bills triggers your brain's satisfaction awareness earlier in the meal.

You taste more intentionally when every dish was a conscious choice rather than an automatic swipe. Card-payers over-order, then feel sluggish and vaguely guilty. Cash-payers order exactly what they want and savor it. That same principle of intentional, painless saving once powered a brilliant bank program your grandparents probably used — one that eliminated holiday debt entirely.

The Christmas Club Account Was Genius

Banks used to offer something called a "Christmas Club" account, and it was quietly brilliant. Starting each January, you'd deposit a small amount — often just $5 or $10 — every week. The money was locked until November. No withdrawals, no exceptions. When the holidays arrived, you had $250 to $500 waiting, earmarked entirely for gifts. No credit card bills in January. No financial hangover. Like the coin jar, it worked because saving was painless and automatic.

Modern financial planners call this concept a "sinking fund," but few people actually set one up. The old version was simpler — zero fees, no app, no decisions. It worked precisely because it removed choice from the equation. But saving money wasn't the only place your grandparents skipped the middleman.

They Knew Every Neighbor's Skill

Your grandparents had something better than TaskRabbit — they had the neighborhood. One neighbor rebuilt carburetors, another prepared tax returns, someone down the street watched kids every Thursday. No platforms, no service fees, no 15-30% cuts disappearing to some company in Silicon Valley. These informal skill-swap networks saved families an estimated $2,000-$4,000 annually in services they never had to pay retail prices for. Think about what you're good at — maybe you cook, maybe you're handy, maybe you're great with dogs.

Here's the insider edge: financial planners are now actively recommending clients rebuild these local exchange networks, calling them one of the most overlooked strategies for reducing household expenses. The barrier isn't skill — it's that we stopped talking to our neighbors. But old-school money wisdom wasn't just communal. The most powerful habit happened privately, at the kitchen table, once a week.

A Weekly Family Money Meeting

Every Sunday evening, fifteen minutes at the kitchen table. That's all it took. Parents would sit down together with one simple goal: get on the same page about money. No spreadsheets, no app dashboards — just three questions. What did we spend this week? What's coming up next week? And what can we skip? Research confirms couples who discuss finances weekly report significantly less financial stress and higher relationship satisfaction. The magic wasn't complexity — it was consistency.

Try it tonight. Set a timer for fifteen minutes, grab a cup of coffee, and walk through those three questions with your partner. You'll catch forgotten subscriptions, overlapping purchases, and upcoming expenses before they become emergencies. Fifteen minutes of honesty replaces months of quiet financial tension. But alignment is only half the equation — what you do with your money *first* matters even more.

Why "Pay Yourself First" Never Fails

Here's the difference between retiring comfortably and working until you physically can't: which bill you pay first. The old-school rule was non-negotiable — before the mortgage, before groceries, before anything, move a fixed percentage into savings. Ten percent was the gold standard. People who save first and spend what's left accumulate nearly three times more wealth than people who spend first and save what's left — even at identical incomes. Same paycheck, completely different futures.

That gap compounds over decades into hundreds of thousands of dollars. This isn't a cute budgeting tip. It's the single habit that determines whether you spend your seventies traveling or terrified. Move the money before you see it, before you can rationalize spending it. Your future self is counting on it. And if this old wisdom already feels familiar, there's a reason for that.

You Already Know More Than Any App

Remember her? Grandma at the kitchen table, envelope in hand, coin jar on the counter, notebook in her purse. She never downloaded a single app. She never watched a financial influencer. And she never once worried about choosing the wrong budgeting platform. You watched her. You absorbed every habit without realizing it. That quiet wisdom has been living inside you this entire time — buried under a decade of marketing that convinced you managing money required a subscription.

You didn't forget how to handle money. You were taught to believe you couldn't do it alone. But you can. You always could. Now there's just one question left — where do you start?

Start With Just One Habit This Week

Pick one. Just one. The sleep-on-it rule before your next purchase. A pocket notebook for one week. A coin jar on your counter. A handwritten grocery list every trip. Or a fifteen-minute Sunday money meeting. That's your whole list. No downloads. No subscriptions. No passwords. No monthly fees. Just one small habit that worked for decades before Silicon Valley decided you needed help.

Start tonight. Start tomorrow morning. Start before you forget this feeling — the one telling you that you already knew this all along. Because the best financial plan isn't an app. It's the one your family already taught you.Disclaimer: This story is based on real events. However, some names, identifying details, timelines, and circumstances have been adjusted to protect the privacy of the individuals involved. The images in this article were created with AI and are illustrative only. They may include altered or fictionalized visual details for privacy and storytelling purposes