Most of us watch the total climb at checkout and wonder where the money goes. Couponing sounds great until you realize it's basically a part-time job. Here's the thing: stores already have built-in savings systems that most shoppers walk right past every single week. No clipping required. Let me show you what you're missing.

You're Already Overpaying Every Week

You know the feeling. You grab the same groceries, the same household basics, the same brands you always buy — and somehow the total keeps climbing. You've probably tried couponing at some point too. The binder, the scissors, the Sunday paper spread across the kitchen table. It lasted maybe two weeks before it felt like a second job. Here's what nobody tells you: you don't need coupons to save thousands.

Stores have built-in savings mechanisms — pricing quirks, hidden policies, markdown rhythms — that most shoppers walk right past every single week. No apps with 47 steps required. Let's start with the trick hiding in plain sight on every shelf tag.

Why Store Layouts Are Against You

You already know stores put milk and eggs in the back corner, forcing you to walk past everything else. That's retail design 101. But here's what makes it personal: research shows the average shopper makes 2.5 unplanned purchases per trip specifically because of how the store routes you through high-margin aisles. At $4-$7 per impulse item, that's roughly $700 a year in stuff you never intended to buy.

The simplest counter-move? Shop the perimeter in reverse — start from the back, grab essentials first, then leave. When your cart already has what you came for, those middle aisles lose their pull. But even the items you *do* plan to buy might be costing more than they should — and the proof is hiding in tiny print right on the shelf.

The Price Tag Trick Nobody Notices

Look at any shelf tag and you'll see two prices. There's the big, obvious one — and then a tiny number tucked in the corner showing the cost per ounce, per count, or per pound. Most shoppers never glance at it, and that's not an accident. Stores frequently shrink that unit price font to near-illegibility. Here's why it matters: the bigger box isn't always the better deal. Sometimes the medium jar of peanut butter costs less per ounce than the family size. Sometimes the "value pack" is quietly more expensive than buying two smaller ones.

A family that starts comparing unit prices on just ten staple items — cereal, coffee, rice, detergent, paper towels — typically saves $400 to $600 a year. No coupons, no apps, just reading the fine print stores hope you'll skip. And those shelf tags have another secret most people have never heard of.

The Markdown Schedule Stores Hide

Here's something store employees know that you probably don't: nearly every major grocery and retail chain follows a predictable markdown schedule. Meat departments typically mark down on Monday mornings. Bakery items drop on specific evenings. Clothing clearance hits on set weekdays. These rhythms repeat like clockwork, week after week, because inventory systems demand it.

The loophole is almost embarrassingly simple. Walk up to any department manager and ask, "When do you usually mark things down?" Most will tell you without hesitation — they have no reason not to. That one question can save you 30-50% on meat, bread, and produce regularly. And asking turns out to be a surprisingly powerful savings strategy that goes far beyond the grocery store.

Ask For the Discount. Seriously.

Here's your new favorite sentence: "Is this the best price you can offer today?" Memorize it. Say it at furniture stores, hotel front desks, electronics counters, even pharmacies. It's polite, non-confrontational, and devastatingly effective. Consumer research shows that simply asking for a discount in non-grocery retail works roughly 70% of the time. Most stores give employees discretionary authority to reduce prices, match competitors, or throw in extras — but only when someone asks.

Try it on your very next purchase over $50. The worst they can say is no, and you're exactly where you started. But what about items you've already bought and paid full price for? Turns out, you might still be owed money.

Price Adjustment Policies Save Hundreds

That TV you bought last month? It's $40 cheaper today — and the store owes you the difference. Most shoppers have no idea that Target, Nordstrom, Best Buy, and dozens of other major retailers offer price adjustment policies within 14 to 30 days of purchase. If anything you bought drops in price during that window, one quick visit to customer service or a chat message gets you the difference refunded to your original payment method.

One woman made checking recent receipts against current sale prices a weekly five-minute habit. In twelve months, she recovered $1,200 — money she'd already spent, returned without giving anything back. That's the definition of found money. But what if the product itself has a flaw most people would overlook?

The "Damaged Box" Loophole at Big Stores

Retail employees know something most shoppers don't: that dented box on the shelf is a negotiation opportunity. When you spot a scratched appliance, torn packaging, or scuffed display model — especially at warehouse clubs and home improvement stores — bring it to a manager and say, "I'd like to buy this, but the packaging is damaged. Can you adjust the price?" That's it. Store managers typically have authority to discount 10-20% on the spot, no approvals needed.

The product inside is identical. The manufacturer's warranty still applies in full. You're simply saving money because a box got bumped on a truck. Electronics, small appliances, and power tools are the sweet spot — that's easily $20-$80 off per item. Now, imagine applying this same insider thinking to something you buy every single month: your prescriptions.

Your Pharmacy Is Overcharging You

The same generic medication — identical pill, identical manufacturer — can cost $8 at one pharmacy and $95 at another just three miles away. That's not a typo. Prescription pricing has almost no transparency, and pharmacies count on you never comparing. A free lookup on GoodRx or similar tools takes thirty seconds and routinely cuts costs by 50-80%. Here's something most people don't realize: warehouse club pharmacies at Costco and Sam's Club are open to everyone. Federal law prohibits requiring a membership to fill prescriptions there.

If you're on three or four medications, this single change could save $1,000-$3,000 a year — money that stays in your pocket instead of padding pharmacy margins. And that Costco detail? It's just the beginning of what you can legally access without a membership.

Costco Without a Membership? It's Legal.

Here's something Costco doesn't advertise: their pharmacy is just the start. Federal and state regulations also keep their optical departments and hearing aid centers open to non-members. Their food court? Accessible without a card at most locations. But the real trick insiders love is the gift card workaround. Have a member friend buy you a Costco Shop Card — even a $10 one. Company policy allows non-members to shop inside and pay with that card, including purchasing additional merchandise beyond the card's balance.

You'll pay a small surcharge — typically 5% — but on bulk staples, cleaning supplies, and household goods, you still come out well ahead of regular retail pricing. These policies exist because of legal requirements and corporate rules that simply aren't promoted. So what about the loyalty programs you already have — are any of them actually worth keeping?

Loyalty Programs That Actually Pay Off

Most loyalty programs aren't worth the mental clutter. But three types earn their place with zero extra effort after signup. First, your grocery store's fuel rewards program. If you're spending $150 a week on groceries — which many families do — you're earning enough fuel points to save $300-$500 a year on gas without changing a single habit. Second, a cashback credit card with rotating grocery categories. Cards like Chase Freedom or Discover give 5% back on groceries during bonus quarters — that's real money back on spending you'd do anyway.

Third, retailer apps like Target Circle or the Walmart app that auto-apply discounts at checkout. No clipping, no scanning barcodes, no hunting for deals. Just download, enroll, and forget. These three programs combined could quietly return $600-$1,000 a year. But knowing when to buy matters just as much as where — and timing your purchases could be the easiest strategy yet.

Why You Should Never Buy on Launch Day

Retail insiders know every product follows a pricing lifecycle — and launch day is always the peak. New clothing drops 25-40% within six to eight weeks as it hits what industry buyers call the "second markdown." Electronics follow a similar curve over two to three months. Remember those markdown schedules from earlier? This is the same principle on a larger scale. The sweet spot isn't the first sale — it's the second price cut, when stores genuinely need the inventory gone.

Holiday décor is the most dramatic example. The week after Christmas, Valentine's Day, or Halloween, stores slash prices 75-90% because that inventory becomes a liability overnight. Patience isn't deprivation — it's a financial strategy with a predictable payoff. And speaking of money you've already spent, there's a generous store policy most people completely waste.

The Return Policy Most People Waste

That jacket that didn't fit right. The skincare product that broke you out. The kitchen gadget collecting dust. You already paid for these things — but that money isn't necessarily gone. Americans leave an estimated $18 billion in returnable purchases sitting in closets every year. The reason? Embarrassment, or assuming it's "too late." It's usually not. Costco accepts returns on most items with no time limit. REI gives you a full year. Sephora and Ulta take back opened cosmetics and skincare.

Target, Walmart, and Nordstrom all offer more flexibility than most shoppers realize. The loophole here isn't complicated — it's keeping your receipts and being willing to walk back through that door. Think of every unused return as cash sitting in a drawer you forgot to open. Now imagine a tool that hunts down savings automatically while you shop online — without you lifting a finger.

The Browser Extension Doing the Work for You

Here's your one-minute setup: go to your browser's extension store, search for Capital One Shopping or Honey, click "Add to Browser," and you're done. That's genuinely it. From now on, every time you reach an online checkout, the extension automatically tests available coupon codes and applies the best one — no searching, no copying and pasting mysterious codes from sketchy websites. You just watch the price drop. But the hidden feature most people miss is price history tracking. Before buying anything, these tools show you whether today's "sale" price is actually lower than last month's regular price.

You'd be surprised how often a 40% off "deal" is really just the normal price dressed up. These extensions strip away that illusion for free. And if you think saving money on things you already buy is satisfying, wait until you hear about items stores are legally required to give you at no charge.

Stores Legally Owe You Free Stuff

Here's something most shoppers have never heard: if an item scans at a higher price than the shelf tag shows, you may be legally entitled to get it free. Michigan's Scanner Law requires stores to pay customers a "bounty" — the difference plus ten times the overcharge, up to $5. Several other states have similar protections. Even where no law exists, major chains like Target, Walmart, and Kroger maintain voluntary policies giving you the first mis-scanned item free.

Remember those tiny unit-price shelf tags from earlier? They matter even more now — they're your proof. Politely tell the cashier, "This tagged at a different price," and ask about their scanning accuracy policy. Most employees will correct it immediately. Some shoppers catch multiple errors weekly. Now imagine combining that awareness with a strategy that saves 30-50% on big-ticket electronics and appliances.

Buying Refurbished Is the Smartest Move

Professionals never pay full price for electronics — they buy manufacturer-refurbished. Apple, Dyson, KitchenAid, and Dell all run official refurbished stores where products are tested, repaired to factory standards, and sold with full warranties at 30-50% off. That $1,000 laptop becomes $600. That $400 vacuum drops to $250. The key distinction insiders know: "manufacturer refurbished" means the original company rebuilt and certified it — virtually no risk. "Seller refurbished" means a random third party handled it, which is a gamble.

Always look for the manufacturer's own refurbished store first. You'll get the same product, same warranty, same performance — just a different price tag. And if you want to stack even more savings on purchases you're already planning, there's a gift card trick that quietly shaves another 5-20% off the top.

The Gift Card Trick Insiders Use

Before making any major purchase, savvy shoppers buy discounted gift cards first. Sites like Raise and CardCash sell gift cards at 5-20% below face value — so a $100 card might cost $85. You're spending money you were already going to spend, just less of it. Now layer this: buy that discounted gift card during a store's sale, and your savings compound. A $200 item on 25% clearance, purchased with a gift card you got for 15% off, drops your real cost dramatically.

Here's another insider move — buy retailer gift cards at your grocery store. Many grocers count gift card purchases toward fuel reward points, so you're stacking savings across two systems simultaneously. Zero extra effort, just a smarter sequence. Speaking of unclaimed savings, there's a much bigger category where most households are quietly losing hundreds every year without realizing it.

Your Insurance Discounts Are Going Unclaimed

Right now, your insurance company likely owes you money — they're just waiting to see if you'll ask. Most auto, home, and health insurance policies include discounts that never get activated: bundling, safe driver, home security systems, paperless billing, loyalty tenure, even age-based reductions. The average household leaves $300-$800 per year unclaimed across their policies. That's not spare change — over five years, it's a vacation or a new appliance fund, vanishing silently.

The fix requires exactly one phone call annually. Ask your agent this specific question: "What discounts am I currently eligible for that aren't applied to my policy?" They have a checklist — make them read it to you. One conversation, potentially hundreds saved every single year. Now let's bring this savings mindset back to the grocery store, where the calendar itself can cut your food bill nearly in half.

Why Buying Seasonal Food Saves a Fortune

Here's a simple framework you can use starting this week. In summer, load up on berries, tomatoes, and stone fruits. Fall means apples, squash, and root vegetables are at their cheapest. Winter is citrus season — oranges, grapefruits, and clementines drop 30-50% compared to summer prices. Spring brings affordable greens, asparagus, and peas. Buying in season doesn't just save money — the produce genuinely tastes better because it hasn't traveled thousands of miles to reach you.

And here's the year-round cheat code: frozen fruits and vegetables, picked and flash-frozen at peak ripeness, are nutritionally equivalent to fresh and cost a fraction of the price. A family shifting even half their produce buying to seasonal patterns saves $500-$1,000 annually. But groceries aren't the only place silent charges are draining your budget month after month.

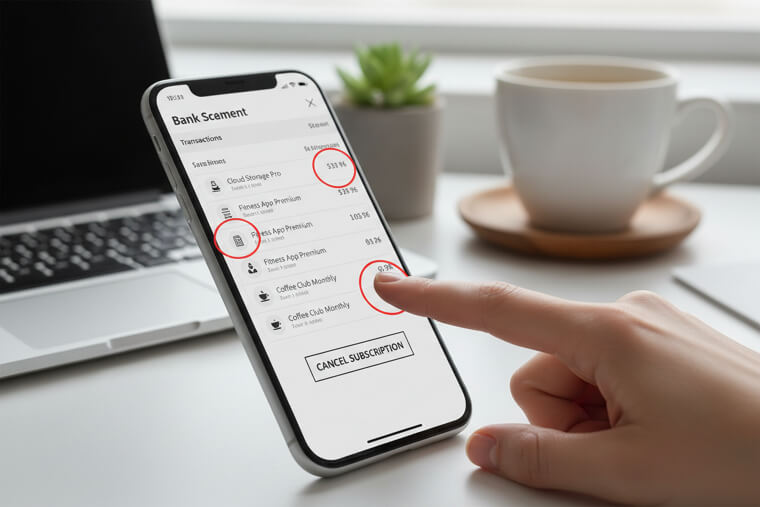

The Annual Subscription You Should Cancel Today

The average American pays for 3-4 subscriptions they've forgotten about — streaming services, free trials that converted, apps they opened once. That quiet drain adds up to $200-$500 every single year, charged while you sleep. But here's the real loophole: don't just cancel — start the cancellation process. The moment you click "cancel," many services panic. Suddenly you're offered 30-50% off for the next six months. Retention is cheaper than finding new customers, so they'll fight to keep you.

Try this today: open your bank statement, circle every recurring charge, and cancel anything you haven't used in 30 days. Services like Rocket Money can scan and cancel forgotten subscriptions automatically. But subscriptions aren't the biggest bill most people overpay without questioning — that distinction belongs to something far more stressful.

Negotiate Every Medical Bill. Every One.

Medical bills are the single most negotiable expense in your life, yet most people pay the first number they see without question. Hospitals and providers routinely reduce bills by 20-50% — they expect patients to negotiate. They have entire departments built around it. Here's your opening line, word for word: "Is there a prompt-pay discount or financial assistance available?" That single sentence unlocks reductions most billing representatives are authorized to offer immediately.

One phone call on a $3,000 hospital bill can erase $600 to $1,500. Think about what that means for your family. You don't need to argue or justify — just ask. The system is designed to reward those who do. And speaking of rewards you've already earned but never collected — there's a whole category of discounts specifically created for your age group.

The Senior and AARP Discounts Nobody Advertises

Here's your checklist — start using these immediately. At restaurants, ask about senior discounts before ordering. Many chains offer 10-15% off starting at just age 55, but you have to ask. At 62, grab the lifetime National Parks pass for $80 — it covers entrance fees forever. Amtrak gives 10% off every trip. Goodwill runs senior discount days offering 25-50% off storewide. And check your county website for property tax exemptions — many states freeze or reduce rates for seniors, saving hundreds annually.

Now, AARP membership costs just $16 a year but unlocks hotel, rental car, and pharmacy discounts easily worth $160-$300. That's a 10-20x return on a membership most people forget they have. Your earned discounts are everywhere — you just have to claim them. And there's another card in your wallet with even more hidden power than you'd ever expect.

Your Library Card Replaces $1,000 in Subscriptions

That dusty library card might be the most powerful savings tool you own. Today's libraries are digital powerhouses most people haven't discovered yet. With a free card, you get Kanopy for streaming thousands of movies, Libby for audiobooks delivered straight to your phone, and PressReader for hundreds of digital magazines — all completely free. Many library systems also lend museum passes, providing free family admission worth $50-$100 per visit. Some cities even run tool lending libraries where you can borrow power tools instead of buying them.

Add it up: replacing Netflix, Audible, magazine subscriptions, and a few museum trips easily saves a family over $1,000 annually. Everything works from your couch — no late fees, no physical books required unless you want them. All these savings strategies are powerful alone, but what happens when you start passing them down to the people you love most?

Teach Your Grandkids This One Habit

Think about who taught you to stretch a dollar. Maybe it was a parent checking prices at the kitchen table, or a grandparent who simply never wasted. That wisdom stayed with you because you watched someone live it. Now you're that person. The most powerful financial lesson you can give your grandkids fits in one sentence: before spending over $50, wait 24 hours and check one other price. That's it. No lecture, no textbook — just a habit that compounds across a lifetime.

When they see you pause, compare, and choose wisely, they absorb something no classroom teaches. You become the person in your family who knows how things really work. And when you start adding up everything you've learned here, the numbers might surprise you.

Small Wins Add Up to Thousands

Let's make this real. Say you save $40 a month from unit pricing, $50 from shopping markdowns, $30 from simply asking for discounts, $35 from fuel rewards, $60 from eating seasonally, and $25 from canceling forgotten subscriptions. That's $240 every single month — nearly $3,000 a year. Pick up just two or three more strategies from this article, and you're looking at $4,000 to $5,000.

That's a vacation with your grandchildren. That's a medical bill that stops haunting you. That's sleeping easier on a Tuesday night knowing there's a cushion. Not one coupon clipped. You already know enough to change your year — but there's one final shift in thinking that ties everything together.

The Best Loophole Is Knowing Your Worth

Here's the truth every store, insurance company, and billing department hopes you never realize: these loopholes aren't hidden because they're illegal or complicated. They're hidden because your not knowing is profitable. Every strategy in this article exists because someone counted on you not asking, not checking, not believing you could. But you can. You've worked too hard — raised families, built lives, shown up every single day — to leave your own money sitting on someone else's counter.

Pick just one strategy this week. Ask for the discount. Check the unit price. Make the call. Notice how it feels to keep what's yours. That feeling? It isn't cheap. It's the smartest thing you'll do all year.Disclaimer: This story is based on real events. However, some names, identifying details, timelines, and circumstances have been adjusted to protect the privacy of the individuals involved. The images in this article were created with AI and are illustrative only. They may include altered or fictionalized visual details for privacy and storytelling purposes